分析文章 | 雷达里奥谈疫情对投资市场的影响:我们对冠状病毒和流行病的早期思考

Our Early Thinking on the Coronavirus and Pandemics

Ray Dalio

Co-Chief Investment Officer & Co-Chairman of Bridgewater Associates, L.P.

First of all let me be clear that I’m a “dumb shit” when it comes to pandemics because what I don’t know about them is more important than what I do know. I, and we at Bridgewater, don’t have a clue as to what extent this virus or “pandemic” will spread, we don’t know where it will spread to, and we don’t know its economic or market impact. However, we do know that major pandemics are one of those really big things that we haven’t really experienced in our lifetimes but have repeatedly happened in other lifetimes and have had big impacts—similar to other big things that are really big deals that haven’t happened in our lifetimes like world wars, ends of monetary systems, or the once-in-a-hundred-years drought or flood. Following my usual approaches I a) want to study a bunch of them to see how they work and b) make sure that our portfolios are either well diversified or hedged so that we don’t have any inadvertent big bets that we don’t have a good likelihood of betting on well.

As for the spreading of this virus, as with any sort of unknown, there are 1) actual events and 2) the expectations of events that get reflected in market pricing. Generally speaking these once-in-a-lifetime big bad things initially are under-worried about and continue to progress until they become over-worried about, until the fundamentals for the reversal happen (e.g., the virus switches from accelerating to diminishing). So we want to pay attention to what’s actually happening, what people believe is happening that is reflected in pricing (relative to what’s likely), and what indicators that will indicate the reversal.

Regarding diversification to protect us against the unknowns, the outbreak of the coronavirus and its effect on markets highlight its importance. China’s stock market is down nearly 10% since the virus took off. Terrible, unimaginable things could happen anywhere. What we don’t know is much greater than what we do know. When you don’t know, the best investment strategy is to be smartly diversified across geographic locations, across asset classes, and across currencies.

Putting This One in Perspective

The main purpose of these Observations is to show you what we have observed going back through time in our attempt to track the evolution of this case in relation to both the archetypical virus pandemic and each of the historical cases (which provide a wide range of variation around the archetypical one). We will also look at the relationships between past pandemics and past economic and market impact of past pandemics, while sorting out the exact impacts.

Recent Past Cases

To look at the last ones and to convey the severity of them, the following table shows past major disease outbreaks comparing mortality rates. As shown by looking at the number of deaths, the last big one—and the only one that was of a large magnitude—was the one that happened almost exactly 100 years ago.

Let’s look at three of the largest cases: H1N1, SARS, and the Spanish Flu. What follows are some observations that we have about them.

Let’s look at three of the largest cases: H1N1, SARS, and the Spanish Flu. What follows are some observations that we have about them.

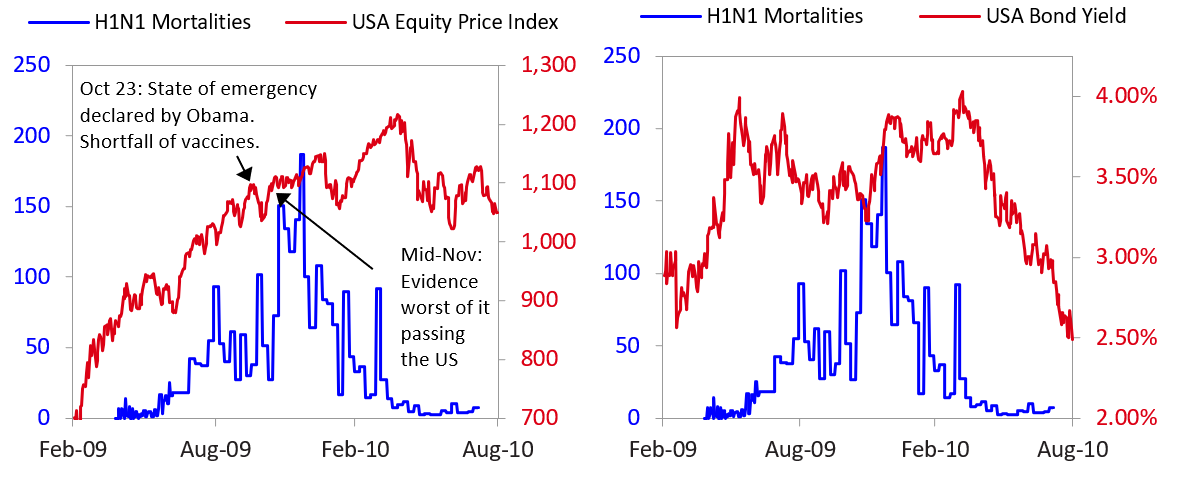

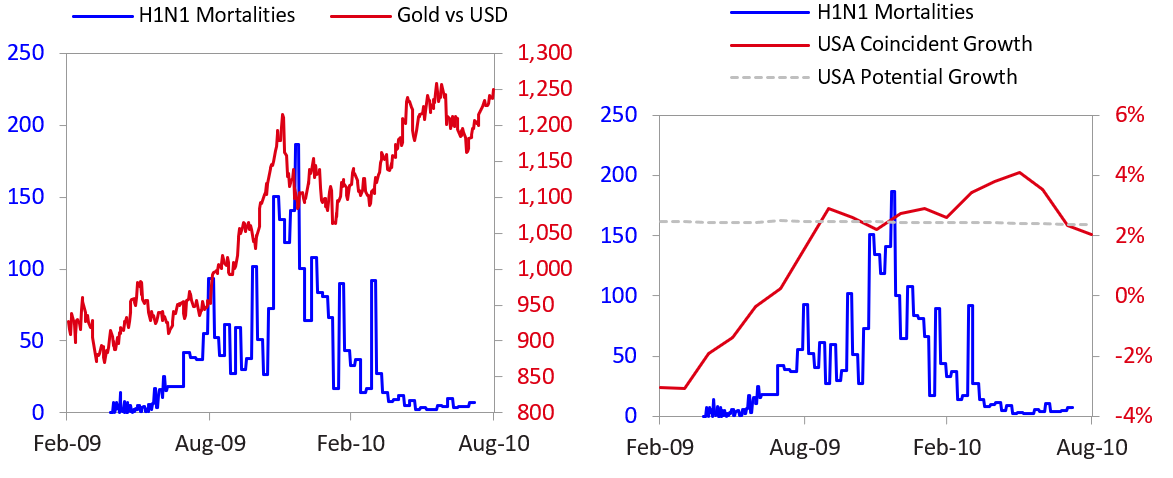

Regarding the first two, which were also the much smaller ones, on the days in which there were big bad headlines about disease outbreaks, the markets acted in a risk-off way that is consistent with falling growth and flight-to-quality—i.e., equities declined, and gold and bonds rose (as we’ve seen over the last couple days). However, these reactions faded and there became no clear and big sustained market moves as other influences such as monetary policies and economic activities that weren’t associated with the virus were much more important. By the way, in looking at those few cases, keep in mind that that wasn’t a big sampling and there were some coincidences that shouldn’t be made too much of—e.g., H1N1 coincided with the beginning of the recovery from the 2008 financial crisis—so one should be cautious about reading too much into the correlations alone.

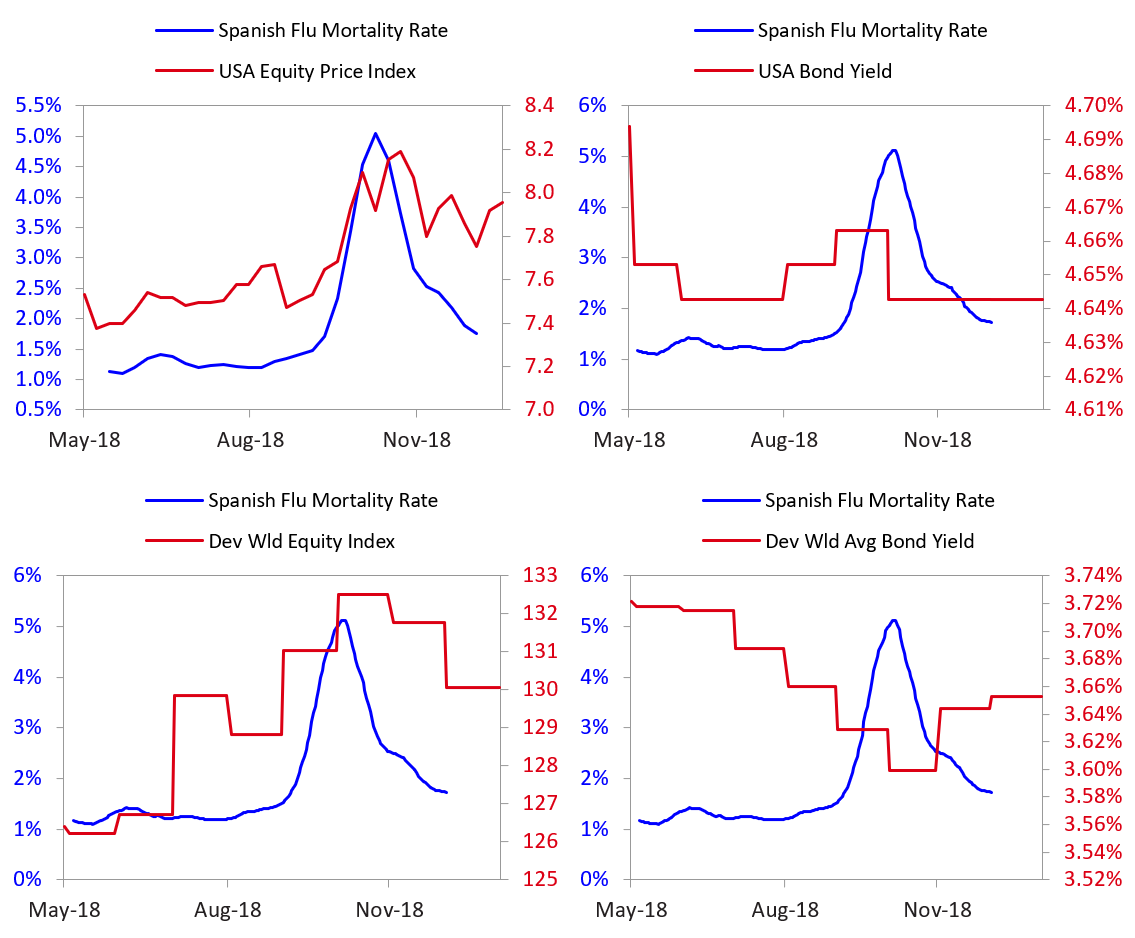

The impact of the larger Spanish Flu epidemic—which was the much bigger one—on markets and economies was much larger.

Let’s look at them individually.

H1N1 (Swine Flu): 2009 to 2010

This outbreak involved a variant of the same virus as in the Spanish Flu of 1918 (H1N1). The first cases were found in Mexico in March 2009. Unlike then and other pandemics, this virus did not disproportionately infect adults older than 60. Estimates of the total death toll range widely (as distinguishing deaths from this disease and regular seasonal flu with certainty requires lab testing), but recent WHO estimates suggest around at least 150,000 deaths, and perhaps multiples of that—significant but not game-changing (by comparison each year 1.25 million people die from auto accidents). The WHO declared an end to the pandemic on August 10, 2010.

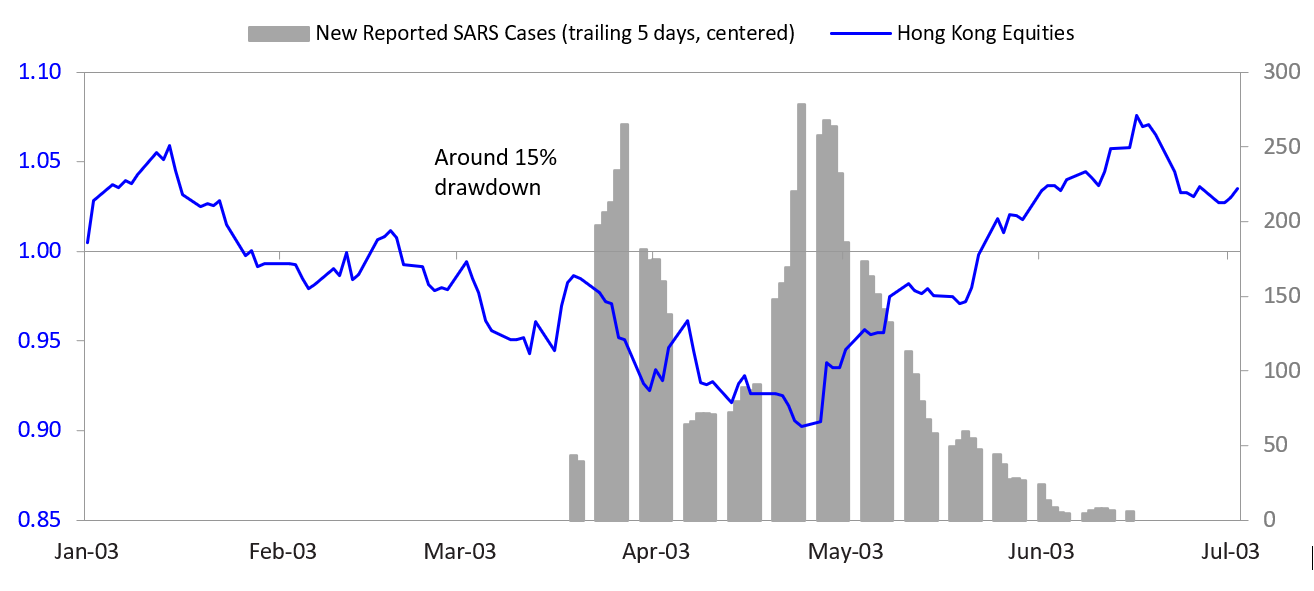

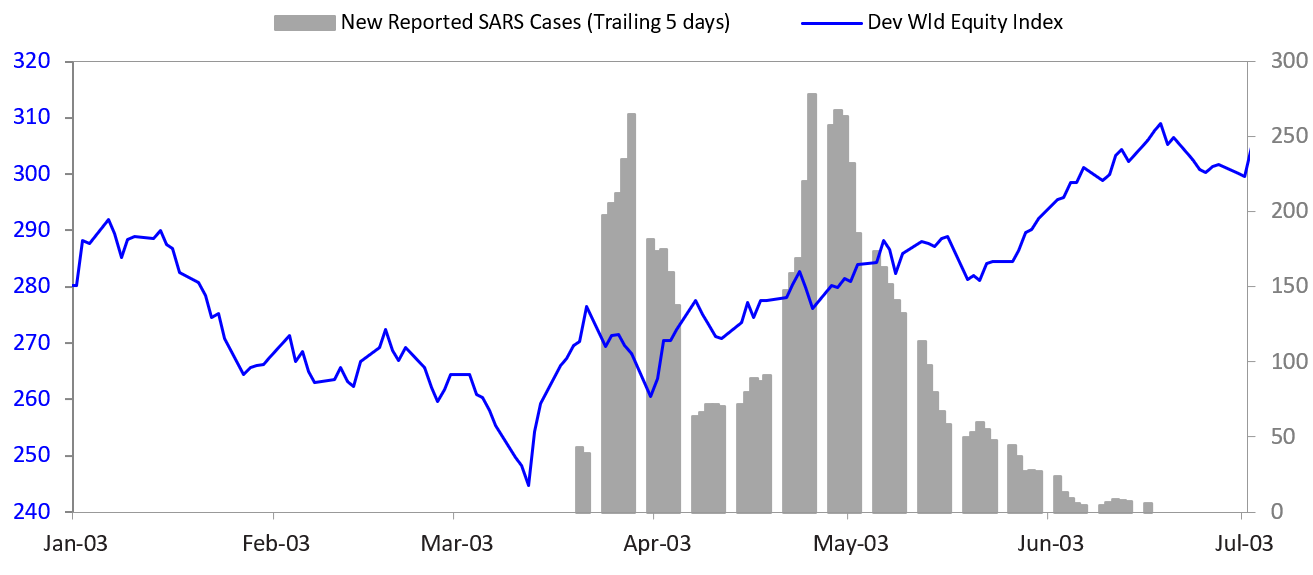

SARS: 2003

The SARS coronavirus was an animal virus that first spread to other animals and eventually infected humans, with the first case being found in the Guangdong province of southern China on November 16, 2002. SARS affected 26 countries, infected around 8,000 people, and caused some 800 deaths. The first cases arrived in Hong Kong in February and spread quickly. In mid-March, the WHO issued a global alert and an emergency travel advisory related to SARS. In late March, the data reporting on new infection cases began (shown in the charts below). On July 9, 2003 the WHO declared the virus was contained, and apart from a brief flare-up in 2004, it remained contained.

You can see the effect in the divergence between the Hong Kong stock market with the world stock market in the charts below. You can see that the Hong Kong stock market was adversely affected by SARS and reversed when the number of SARS cases peaked and started to go down. This is all logical and would be the type of market action we would expect if the coronavirus crisis remains concentrated in China. In other words, we would expect its effects to be greater on the Chinese and Hong Kong markets than on the world markets, and we would expect these effects to diminish as the number of new cases also starts to diminish.

Spanish Flu: 1918

This was the deadliest pandemic in modern history. The first patient was discovered on March 4, 1918 at Camp Funston, Kansas, though the virus was thought to have originated in China. A cook at an army base reported to the infirmary with flu-like symptoms—a low-grade fever and a mild sore throat. By noon, 107 people were sick. Within two days, 522 people were sick. Within a week, every state in the US was affected. Then it spread across the Atlantic and, by mid-April, had spread to China and Japan. By May, it was virtually everywhere.

Importantly, the outbreak occurred in the midst of World War I. This contributed to the outbreak (as malnutrition, poor hygiene, and dense accommodations of soldiers provided ideal conditions for the disease to spread). It has been estimated that nearly 500 million people were infected and approximately 50 million were killed (although estimates vary). In the end, it killed far more people than World War I. After about 18 months, it passed.

The impacts of the war and the pandemic are hard to disentangle in market and economy charts, but it looks like positive developments in the war (the peak of the disease roughly coincided with the ending of the war) were overshadowed by the pandemic, marking the end of an equity rally. Further, a Federal Reserve Bank of St. Louis report looked through newspapers of the period to triangulate the economic impacts of the flu. The report found headlines that pointed to a very sharp slowdown in the US, as we’d expect. For example:

Fifty percent decrease in production reported by coal mine operators”

“Influenza Crippling Memphis Industries”

“Merchants in Little Rock say their business has declined 40 percent. Others estimate the decrease at 70 percent.”

“The retail grocery business has been reduced by one-third”

Again, these conditions happened at the same time as World War I ended, and not many monthly economic statistics were available, so it’s difficult to clearly see the impact on the economy and to disentangle the pandemic’s impact on the markets from the impacts of war developments and other policy influences.

Again, these conditions happened at the same time as World War I ended, and not many monthly economic statistics were available, so it’s difficult to clearly see the impact on the economy and to disentangle the pandemic’s impact on the markets from the impacts of war developments and other policy influences.

How the Coronavirus Outbreak Compares

Here are some notable facts.

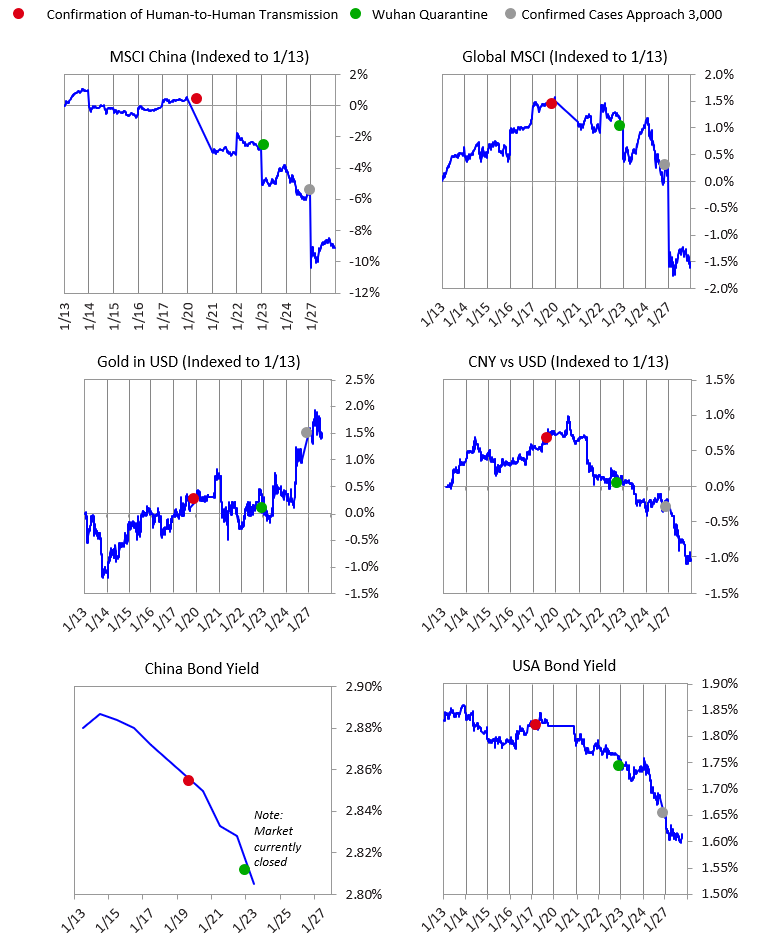

The first case was observed in early December and, according to the WHO on Sunday, a total of 2,014 cases of infection have been reported globally. Of those:

1,985 were reported from Greater China, and 29 from outside China.

Of those 29, 26 cases were of people who traveled to Wuhan. Two of the remaining three had close contact with people who caught the disease in Wuhan (there isn’t enough information on the third case).

324 cases resulted in a person being severely ill (per WHO definition), just over 15%.

56 deaths have been reported, around 2.5% to 3% (compared to an ultimate fatality rate of just under 10% for SARS). These have principally been in older patients or those with pre-existing health problems.

The latest figures reported by Chinese state media as of this writing are 2,844 cases and 81 deaths.

So far, China’s response is much more transparent and decisive compared to the SARS outbreak, which affects both the statistical comparison and the rate of dealing with the problem. Because the Chinese government reported the disease faster to the WHO, it imposed quarantine and other prevention measures earlier. The WHO has praised China’s swift response because of its beneficial effects on containment.

The following charts show market action over the last couple of weeks, with the dots noting some important developments. Over the last several days, the markets have seen strong falling growth and flight-to-quality market action, as shown in the charts below. Equities have sold off globally, while bonds, gold, and the dollar versus the yuan have rallied.

These are just our preliminary observations. We expect to do a lot more homework that will give us a richer perspective, which we will share with you as we develop it.

Disclaimer:

Bridgewater Daily Observations is prepared by and is the property of Bridgewater Associates, LP and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives or tolerances of any of the recipients. Additionally, Bridgewater's actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing and transactions costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This report is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned.

Bridgewater research utilizes data and information from public, private and internal sources, including data from actual Bridgewater trades. Sources include the Australian Bureau of Statistics, Bloomberg Finance L.P., Capital Economics, CBRE, Inc., CEIC Data Company Ltd., Consensus Economics Inc., Corelogic, Inc., CoStar Realty Information, Inc., CreditSights, Inc., Dealogic LLC, DTCC Data Repository (U.S.), LLC, Ecoanalitica, EPFR Global, Eurasia Group Ltd., European Money Markets Institute – EMMI, Evercore ISI, Factset Research Systems, Inc., The Financial Times Limited, GaveKal Research Ltd., Global Financial Data, Inc., Haver Analytics, Inc., ICE Data Derivatives, IHSMarkit, The Investment Funds Institute of Canada, International Energy Agency, Lombard Street Research, Mergent, Inc., Metals Focus Ltd, Moody’s Analytics, Inc., MSCI, Inc., National Bureau of Economic Research, Organisation for Economic Cooperation and Development, Pensions & Investments Research Center, Renwood Realtytrac, LLC, Rystad Energy, Inc., S&P Global Market Intelligence Inc., Sentix Gmbh, Spears & Associates, Inc., State Street Bank and Trust Company, Sun Hung Kai Financial (UK), Refinitiv, Totem Macro, United Nations, US Department of Commerce, Wind Information (Shanghai) Co Ltd, Wood Mackenzie Limited, World Bureau of Metal Statistics, and World Economic Forum. While we consider information from external sources to be reliable, we do not assume responsibility for its accuracy.

The views expressed herein are solely those of Bridgewater as of the date of this report and are subject to change without notice. Bridgewater may have a significant financial interest in one or more of the positions and/or securities or derivatives discussed. Those responsible for preparing this report receive compensation based upon various factors, including, among other things, the quality of their work and firm revenues.